Key Issue News

May in the Balance

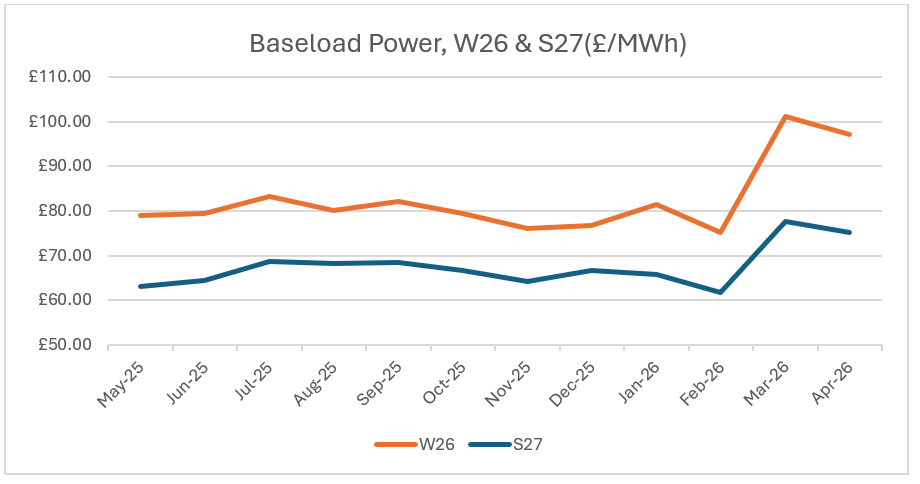

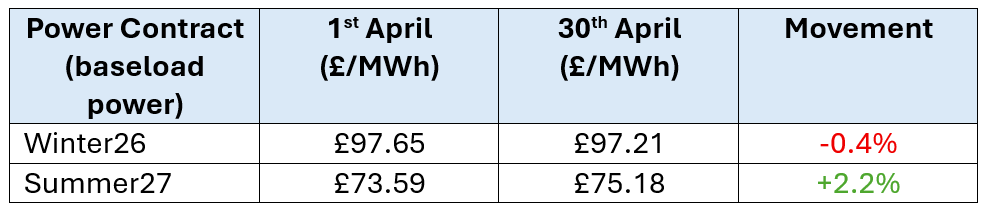

Power markets ended April broadly unchanged, settling into a more stable trading range and showing reduced sensitivity to headline-driven volatility. The month began with a fragile two-week ceasefire that provided some limited relief; however, negotiations in the region remain unresolved. Crucially, the Strait of Hormuz still remains restricted and the long term impacts of this are becoming increasingly apparent. Tensions escalated again toward the end of April, but warmer temperatures and stable wind forecasts helped to contain price volatility.