Global LNG supply chains now have great uncertainty, with Iran-controlled Strait of Hormuz effectively closed and Qatar forced to halt LNG production after targeted attacks. The demand for U.S. LNG intensifies, as Europe and Asia compete desperately for limited cargoes. Gas prices have catapulted, and power markets are frantically tracking the spike. The market remains reactive as strikes continue across the Middle East, so volatile that some suppliers have stopped pricing altogether.

Power

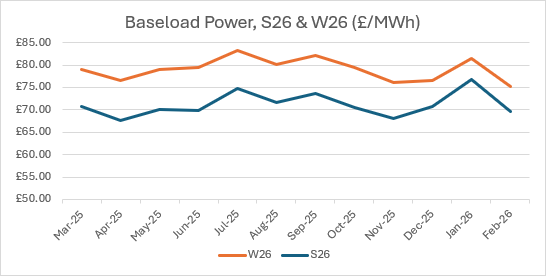

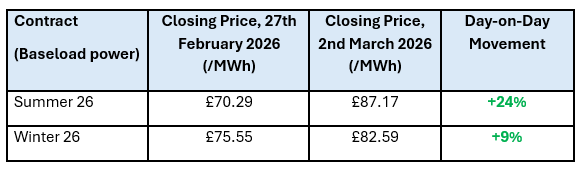

The closing price for February does not take into account the US-Iran conflict that began on the 28th February. The summer26 contract closed higher than winter26 on 2nd March.

Gas

LNG supply remained strong throughout February, though recent geopolitical developments threaten this. 80% of UK and Europe’s LNG imports were sourced from the US in February. Now gas supply is disrupted through the Strait of Hormuz, the region accounts for almost a fifth of global LNG supply, predominantly to Asia. Increased competition between Europe and Asia for US LNG supply, could see significant uplift in markets to attract LNG from US and replenish already depleted storage across UK and Europe.

Looking ahead

- Markets will closely watch conflict in the Middle East, volatility expected

- Global LNG supply expected to be tighter

- UK and Europe storage levels need to be replenished before next winter

FiT Tariff changes 2026

The government has proposed changing the way the Feed-In Tariff (FiT) scheme is indexed to inflation.

They are proposing that FiT tariff rates are to be linked to Consumer Price Index (CPI) rather than Retail Price Index (RPI).

The consultation is ongoing, and once completed, the FiT tariffs for 2026-27 will be published.

The Greenspan Agency produce this report on a best endeavours basis, and it has been supplied for your interest; this report should not be relied upon for decision making. If you have any queries about the content in this report, please contact hana@greenspanenergy.com

Contact Alba Energy